.jpg?VGhlIFBlcmZlY3QgU2xvdC1pbijmraPnoa4pLmpwZw==)

BLOCKCHAIN HAS THE POTENTIAL TO OFFER EFFICIENCIES AND IMPROVEMENTS IN MANY OF THE FOLLOWING AREAS:

Supply-chain monitoring for greater transparency into complex supply chains where delays and sourcing constraints impact production and profitabilityIdentity management for when it is important to know who is taking an action and what their credentials are, including attorneys, auditors, engineers and technicians

Asset tracking to monitor equipment movements or intermodal logistics across carriers

Quality assurance that can look across a production life cycle to gauge qualifications, quality, patterns of defects, etc.

Engineering design for long- duration, high-complexity products, for which delays in sharing updated engineering specifications or parts can increase rework and delay final delivery.

Regulatory compliance enhanced by indelible records of actions taken, assets’ movements evidenced by permissioned consensus.

Materials provenance and counterfeit detection to reduce the $4.2 trillion impact of counterfeiting and piracy on the global economy by 2022, as cited by World Trademark Review

Blockchain-powered solutions can bring together all of this information, delivering significant value for industrial companies, and can also help unlock the full potential of other advanced technologies like augmented reality, Internet of Things (IoT) and 3D printing

Smart contracts

Many of these functions can be automated through smart contracts, in which lines of computer code use data from the blockchain to verify when contractual obligations have been met and payments can be issued. Smart contracts can be programmed to assess the status of a transaction and automatically take actions such as releasing a payment, recording ledger entries, and flagging exceptions in need of manual intervention.

Traceability

If a company discovers a faulty product, the blockchain enables the firm and its supply chain partners to trace the product, identify all suppliers involved with it, identify production and shipment batches associated with it, and efficiently recall it.

Accounts payable

Blockchain can improve accuracy and efficiency in accounts payable management, an elaborate process that involves invoicing, reconciling invoices against purchase orders, keeping track of terms and payments, and conducting reviews and approvals at each step. Even though Enterprise Resource Planning (ERP) systems have increased automation in these areas in recent years considerable manual intervention is still needed. And since neither of the transacting firms has complete information, conflicts often arise.

Cross-border trade

Cross-border trade involves manual processes, physical documents, many intermediaries, and multiple checks and verifications at ports of entry and exit. Transactions are slow, costly, and plagued by low visibility into the status of shipments. Blockchain can increase transparency, verification and speed of processing throughout the chain of events.

DEFINING BLOCKCHAIN

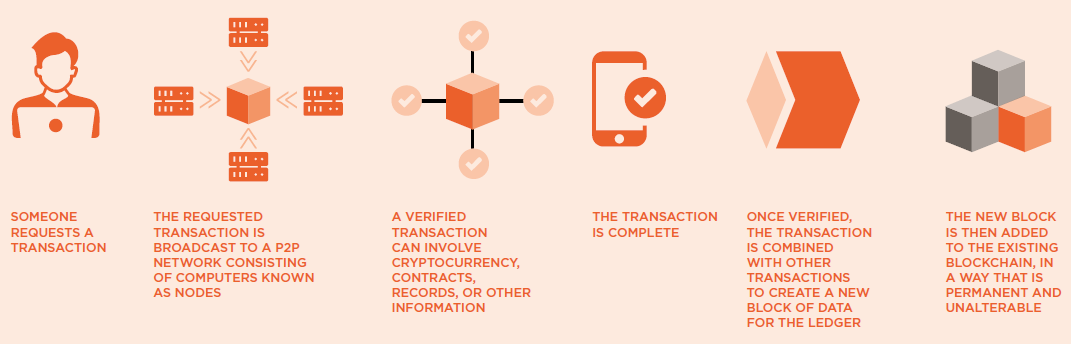

Blockchain is best known as the secure digital system behind bitcoin, the digital currency that operates independently of a central bank. Blockchain works as a distributed, or decentralised ledger, a digital system that records transactions among multiple parties in a verifiable, tamperproof way. Rather than being held in a single, centralised location, the blockchain is held by all the users in a network. While its use outside the finance world is still in the exploratory and developmental stages, manufacturing players are recognising that many elements of blockchain may be integrated into their operations to improve efficiency, security and transparency. To understand why this is, let’s look more closely as how a blockchain works.How blockchain works

In general, all the users in the network, also known as network nodes, have copies of the same ledger. Transactions on a blockchain do not have to be financial—they simply represent a change in state for whichever data point the blockchain’s stakeholders want to track. A blockchain is valuable partly because it comprises a chronological string of blocks integrating all three types of activities in a supply chain: information, inventory and financial, capturing details that are not recorded in a traditional financial-ledger system. Moreover, each block is encrypted and distributed to all participants, who maintain their own copies of the blockchain. Thanks to these features, the blockchain provides a complete, trustworthy, and tamperproof audit trail. When blockchain record keeping is used, assets such as units of inventory, orders, loans, and bills of lading are given unique identifiers, which serve as digital tokens. Additionally, participants in the blockchain are given unique identifiers, or digital signatures, which they use to sign the blocks they add to the blockchain. Every step of the transaction is then recorded on the blockchain as a transfer of the corresponding token from one participant to another. Since participants have their own individual copies of the blockchain, each party can review the status of a transaction, identify errors, and hold counterparties responsible for their actions. No participant can overwrite past data because doing so would entail having to rewrite all subsequent blocks on all shared copies of the blockchain.

How can blockchain in industry work in practice?

Simple blockchains can work well internally for a large manufacturer, by coordinating across its multiple internal ERP systems. When setting up a blockchain to manage supply chains with external partners, the partner companies have to take into consideration the security of their own data. One solution would be for the companies in question to agree to centralize their data on production and inventory-allocation decisions in a common repository. But this would require a huge level of integration. All involved companies would have to trust the others with their data and accept centralized decisions, regardless of whether they are partners or competitors, a solution that few would accept.A more practical solution is for participating companies to share their inventory flows on a blockchain and allow each company to make its own decisions, using common, complete information.

Part of the appeal of using blockchain to enhance supply chain efficiency and speed is that these applications, much like those for improving traceability, require participating companies to share only limited data—in this case, just inventory or shipment data.

It’s important to note that the encrypted linked list or chainlike data structure of a blockchain is not suited for fast storage and retrieval—or even efficient storage. And each link in the chain requires approval from all network partners before the step can be completed.

So a blockchain would not replace the broad range of transaction-processing, accounting, and management-control functions performed by ERP systems, such as invoicing, payment, and reporting. Instead, the blockchain would interface with legacy systems across participating firms. Each firm would generate blocks of transactions from its internal ERP system and add them to the blockchain. This would make it easy to integrate various flows of transactions across firms.

Human error and malicious behaviour

Even when a blockchain record is secure, there is still the danger that a contaminated or counterfeit product might be tagged and introduced into the supply chain, either in error or by a corrupt actor. Another danger is inaccurate inventory data resulting from mistakes in scanning, tagging, and data entry.

Companies are addressing these risks in three ways. First, they are stringently conducting physical audits when products first enter the supply chain to ensure that shipments match blockchain records. Second, they are building distributed applications, called dApps, that track products throughout the supply chain, check data integrity, and communicate with the blockchain to prevent errors and deception. If a counterfeit or an error is detected, it can be traced to its source using the blockchain trail of the transactions for that asset. Third, companies are making the blockchain more robust by using IoT devices and sensors to automatically scan products and add records to the blockchain without human intervention.

Best practices for blockchain solutions

Blockchain solutions can create value for industrial companies in all the ways discussed above. But that does not mean that is the right solution for all companies and industrial manufacturing sectors. By focusing on four key areas early in their blockchain efforts, companies can set themselves on a path toward successful execution.

Make the business case

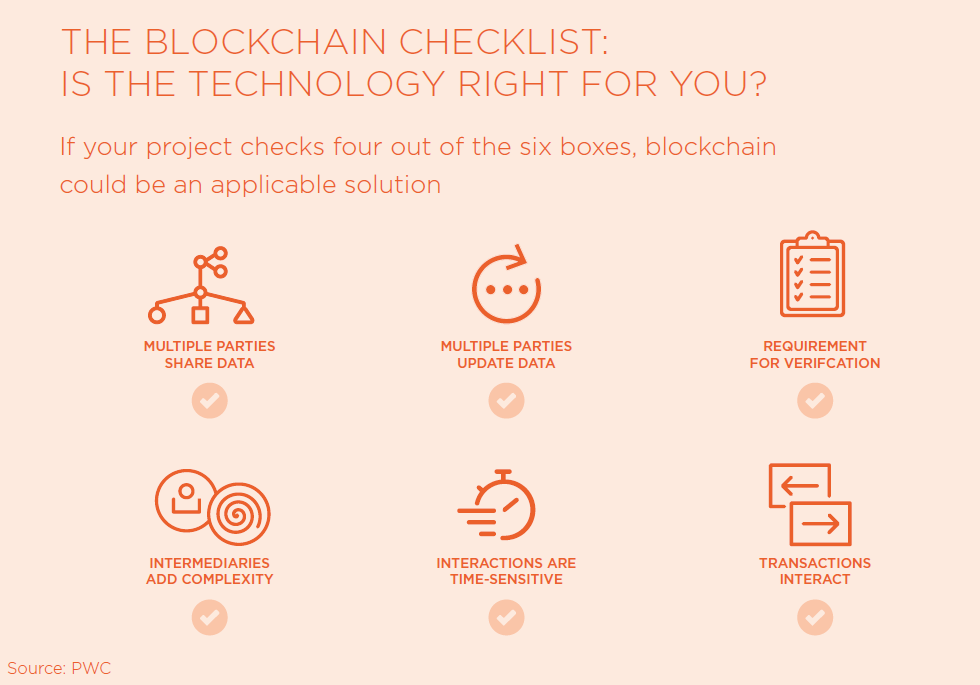

Blockchain needs to be a strategic fit. When there’s a need for different parties to share and update data, when time is of the essence and trust between parties is needed but intermediaries add too much complexity, then blockchain-based solutions can be very effective. But if none or only one or two of those types of challenges are present, then other solutions may be better placed.

Build an ecosystem

Bringing together a group of stakeholders to collectively agree on a set of standards that will define the business model is perhaps the biggest challenge in blockchain. Participants have to decide the rules for participation, how to ensure that costs and benefits are fairly shared, what risk and control framework can be used to address the shared architecture, and what governance mechanisms are in place, including continuous auditing and validation, to ensure that the blockchain functions as designed.

Design deliberately

Much consideration must be given to a blockchain’s design. Will it be permissionless, allowing anyone to initiate and view transactions, or permissioned, restricting access to certain parties? No matter which model is chosen, it’s important to include cybersecurity, compliance, audit and legal specialists in important design decisions from the beginning.

Navigate and seek to shape regulatory uncertainty

Regulators, elected officials and industry groups around the world are still evaluating potential responses to the increasing prevalence of blockchain enabled solutions. It is important to engage with these players, to make the case that blockchain technology can be trusted. Blockchain’s potential for transparency, as well as the immutable record it creates, could make it a powerful tool for regulators.

Conclusions

As blockchain is integrated more and more into the factories and supply chains of the future, the improvements in speed of processes, accuracy and traceability of data, quality control and security all have the potential to impact on staff levels and working practices. While automation, aided by blockchain, may reduce the necessity for worker numbers in certain roles, the need for highly skilled staff to manage the digitised processes will increase. Additionally, in many cases, blockchain is an aid to efficiency, not a replacement for necessary human intervention, which will be required in the foreseeable future for tasks such as auditing and essential communication between partners.

Copyright © Homa 2023

All rights reserved